Applications under family classes: Assessing the sponsor

On this page

- Legislative requirements for the sponsor

- Sponsors residing abroad

- Multiple applications

- Sponsorship bars

- Financial requirements

- Co-signers

- Sponsorship default

- Sponsorship withdrawal

- Assessing a sponsor’s eligibility

- Sponsorship by Canadian citizens living abroad

- Sponsorship ineligibility identified at the permanent resident processing stage

Legislative requirements for the sponsor

Sponsorship provisions in the Immigration and Refugee Protection Act (IRPA) and the Immigration and Refugee Protection Regulations (IRPR)

Relatives who are not eligible to be sponsored under the family class

A sponsor must be a Canadian citizen, permanent resident or Status Indian who

- is at least 18 years of age

- resides in Canada (except in a specific circumstance, see Sponsors residing abroad)

Note: A Status Indian is a person who is registered or entitled to be registered as an Indian under Canada’s Indian Act. Status Indians were unintentionally omitted from the list of persons who may sponsor a foreign national in A13 (who may sponsor). They are administratively included as persons who can sponsor under the family class.

All sponsors must:

- meet the legislative requirements

- submit complete sponsorship applications containing all necessary forms and supporting documents listed in the Document Checklist for the applicable family class program or category [R10]

- sign an IMM 1344 Application to Sponsor, Sponsorship Agreement and Undertaking

- not be subject to a sponsorship bar [R133(1)]

Sponsors must indicate in Q1 on the IMM 1344 whether they wish to proceed with the sponsorship even if they do not meet the requirements to sponsor. If not, a sponsor may withdraw the sponsorship application and receive a refund of all but the sponsorship processing fee. If, however, the sponsor indicates that they wish to proceed, the applications will be sent to the processing office for assessment and final decision.

Sponsors residing abroad

Sponsors who are Canadian citizens living outside Canada may sponsor their spouse, common-law partner, conjugal partner or dependent child (provided that child does not have dependent children of their own). In such cases, an officer must be satisfied that the sponsor will return to reside in Canada once the family members they sponsor become permanent residents of Canada [R130(2)]. Sponsors who are Canadian citizens living outside Canada cannot sponsor their parents or grandparents.

A permanent resident of Canada residing abroad is not eligible to submit a family class sponsorship.

Multiple applications

A sponsor who has filed a sponsorship application on behalf of a foreign national cannot submit another sponsorship application on behalf of the same person if a final decision has not been made on the application for permanent residence submitted with the first sponsorship [R10(5)]. This also applies where a final decision on an appeal has not been made by the Immigration Appeal Division (IAD) on an application for permanent residence that had been refused.

A sponsor is allowed to submit more than one sponsorship application at the same time for different family class relatives, provided that, where applicable, the minimum necessary income (MNI) requirements are met for the total number of persons involved. See Financial requirements for more information.

A sponsor who is applying to sponsor divorced parents/grandparents (and any eligible dependants) must submit 2 separate applications. If the parents/grandparents are still married, even if separated, the sponsor must submit a single application unless one of the parents/grandparents (meaning the principal applicant or the separated spouse) is in a common-law relationship with another person, as per the common-law partner definition in R1(1). In this case, the sponsor should submit 2 applications to sponsor each parent/grandparent separately, along with any eligible dependants.

Note: “Legally separated†is not a recognized relationship status in the Immigration and Refugee Protection Act or its applicable Regulations.

Sponsorship bars

The sponsor and co-signer, if applicable, are required to answer questions in the Sponsor Eligibility Assessment and Co-signer Eligibility Assessment sections of the IMM 1344 designed to assist an officer in determining whether they are subject to a sponsorship bar which would render them ineligible [R133(1)].

If information provided by the sponsor or co-signer on the IMM 1344 – or information that comes to Immigration, Refugees and Citizenship Canada’s (IRCC) attention during processing – suggests that they may be subject to a sponsorship bar, an officer needs to make an informed assessment of the circumstances.

The officer is advised to:

- verify information received with reliable sources

- where necessary, request that the sponsor provide additional information

Where an interview is deemed necessary, the case processing centre (CPC) liaises with an appropriate local IRCC office to arrange one.

Sponsors are not eligible to sponsor if they are subject to any of the bars shown below. Similarly, co-signers who are subject to any of these bars are not eligible to co-sign, and while they will continue to be counted in the family size, their income cannot be used in assessing whether the sponsor meets the MNI requirement. Quebec sponsors are exempt from certain bars.

Learn more:

Financial requirements

- Assessing minimum necessary income

- Foreign sources of income

- Persons counted in family size

- How to count family size with separated spouses

- How to calculate family size for parent and grandparent applications on a year-by-year basis

- Exception to minimum necessary income requirement

- Financial requirements for sponsors living in Quebec

- Quebec case at the time of filing, but sponsor relocates outside of Quebec

- Reassessment of financial circumstances

- Income requirements for sponsoring parents and grandparents

- Income requirements for sponsoring “other relativesâ€

- Application of the temporary public policies of the minimum income requirements for the 2020 and 2021 taxation years

- Duration of sponsorship undertakings

- Duration of undertakings – Quebec

Assessing minimum necessary income

By signing an undertaking, all sponsors promise to give financial support for the basic needs of the people being sponsored.

IRCC assesses whether or not the sponsor has a total income that is equal to or greater than the MNI that sponsors and a co-signer (where applicable) must meet to satisfy IRCC that they are able to provide the basic requirements, e.g. food, clothing, and shelter for themselves, the person(s) being sponsored and any other persons for whom they are responsible (R2).

The MNI is based on Statistics Canada’s low income cut-off (LICO) level, which establishes the annual income level at which a family may have to spend a greater portion of its income on the basics (food, clothing and shelter) than the average family of similar size.

Where the MNI requirements are applicable, sponsors must prove that they have the financial means to support their relatives for the duration of the undertaking specified in R132(1), from the date a signed form IMM 1344 – as a part of a complete application – is received from the sponsor.

The sponsor is expected to do all of the following:

- completes the Financial Evaluation [IMM 1283E (PDF, 2.7Â MB)] , listing all income

- may include a spouse’s or common-law partner’s income to meet the MNI, where applicable

- provides evidence of financial resources

- provides evidence of any social assistance payments received

If a sponsor is unable to meet financial requirements on their own, they may include information on the financial resources of their spouse or common-law partner provided that person co-signs the sponsorship application, where applicable. A sponsor cannot pool financial resources with other relatives in order to meet the MNI.

The undertaking signed by the sponsor (and the co-signer, if applicable) is in effect from the date the sponsored family member becomes a permanent resident. The MNI must be met from the date on which the sponsorship application is signed until the date the sponsored family member becomes a permanent resident.

Foreign sources of income

Foreign income that is declared to the Canada Revenue Agency (CRA) and appears on a Notice of Assessment (NOA), or an equivalent document as issued by the Minister of National Revenue, is counted toward income for the purpose of meeting the MNI. For example, a sponsor or a co-signer who lives in Canada and commutes to the United States (U.S.) for work can count their income earned in the U.S. for the purposes of meeting the MNI provided it is declared income to the CRA and appears on their NOA [R134(1)(a) or R134(1.1)(a)].

For sponsors and co-signers of parent and grandparent applications, only income declared to the CRA that appears on their NOA, or an equivalent document as issued by the Minister of National Revenue, may count toward income for the purpose of meeting the MNI [R134(1.1)(a)]. For other family class sponsors and co-signers who need to meet an income requirement, if the sponsor and/or co-signer does not produce an NOA (or an equivalent document as issued by the Minister of National Revenue) or their income on the NOA is less than the MNI, only the sponsor and/or co-signer’s Canadian income earned during the 12-month period preceding the date of filing of the sponsorship application may be considered [R134(1)(c)].

Persons counted in the family size

In assessing whether a sponsor – and co-signer, if applicable – meets the financial criteria for sponsorship, family size is determined by counting the total number of persons on a year-by-year basis (please refer to How to calculate family size for parent and grandparent applications on a year-by-year basis). The following persons are to be counted in the family size:

Sponsor and their family members

- the sponsor

- the sponsor’s spouse (which might include a separated spouse) or common-law partner

- dependent children of the sponsor

- the dependent children of the dependent children

- the dependent children of the sponsor’s spouse or common-law partner

- the dependent children of the dependent children

Children who meet the definition of a dependent child must be included in the calculation even if the sponsor does not have custody or does not provide child support. This ensures the MNI is met in the event that custody arrangements change during processing.

The sponsored principal applicant and their family members

- the sponsored principal applicant (foreign national)

- the sponsored principal applicant’s spouse (including a separated spouse unless either spouse is in a common-law relationship with another person) or common-law partner

- dependent children of the principal applicant

- the dependent children of the dependent children

- the dependent children of the principal applicant’s spouse or common-law partner

- the dependent children of the dependent children

Family members must still be included in the calculation of family size even if they are not coming to Canada and even if the family members are permanent residents of Canada or Canadian citizens. This follows the definition of “minimum necessary income†found in R2.

Persons from undertakings in effect and their family members

- The number of persons the sponsor has previously sponsored (or acted as a co-signer for) for whom the duration of the undertaking [R132] remains in effect

- their family members, whether or not they were included in the undertaking

- The number of persons the co-signer has previously sponsored (or acted as a co-signer for) for whom the duration of the undertaking [R132] remains in effect

- their family members, whether or not they were included in the undertaking

Undertakings include those from family class and refugee resettlement sponsorships and take effect on the day on which a foreign national becomes a permanent resident. The CPC must review the Global Case Management System (GCMS) to confirm if the sponsor or co-signer has previously sponsored any persons. Officers should make a note in the GCMS of any person sponsored – or co-signed for – who is still being processed and has not yet become a permanent resident. If a sponsored person becomes a permanent resident while a sponsor or co-signer has another sponsorship application in process, the visa officer can request a sponsorship re-assessment, as the family size may have increased.

Officers cannot count the same individuals twice in the family size count. For example, a sponsor has previously sponsored their spouse with an undertaking that is still in effect. The sponsor is now sponsoring their parents to come to Canada, but because the sponsor’s spouse is already counted in the family size (since they are the sponsor’s spouse), the spouse would not be counted again, even though the undertaking is still in effect.

In order to help officers count the family size, the following summary sheet is available.

How to count family size with separated spouses

In the case of a principal applicant who is separated from their spouse, the principal applicant’s separated spouse is considered a “family memberâ€, as per paragraph R1(3)(a), since they are still legally married until they are divorced. However, it should be noted that there could be situations in which subparagraph R5(b)(ii), which details excluded relationships, applies to a foreign national (i.e. the principal applicant). A separated spouse of a foreign national must be counted for the calculation of the MNI unless the spouse has lived separate from the foreign national for at least one year and is the common-law partner of another person. For clarity, either the foreign national (i.e. the principal applicant) or their separated spouse may be the common-law partner of another person.

For sponsors and co-signers who have a separated spouse, a person who is married to another person will continue to be the “spouse†of that person within the meaning of subsection R132(5) until such time that a divorce granted in Canada under the Divorce Act takes effect or, if the divorce was granted outside of Canada by a competent authority, it is recognized pursuant to the Divorce Act. For these reasons, separated spouses of sponsors and co-signers who are permanent residents of Canada or Canadian citizens must be included in the family size count when assessing if the sponsor (and co-signer) meet the income requirement for family class applications. If the sponsor’s separated spouse is a foreign national, an officer should assess whether subparagraph R5(b)(ii) applies.

If a sponsor is separated from their spouse, and their spouse is a permanent resident of Canada or a Canadian citizen but is also in a common-law relationship with another person, their common-law partner does not count toward the family size count. For clarity, the separated spouse counts toward the family size count, but the common-law partner does not.

How to calculate family size for parent and grandparent applications on a year-by-year basis

The Regulations provide that a sponsor’s family size and, in turn, the MNI, must be assessed on a year-by-year basis for each of the 3 taxation years immediately preceding the date of receipt of the sponsorship application, including any increases (for example, birth, marriage, new common-law relationships, and so on) or decreases (for example, death, divorce, end of common-law relationships, end of an undertaking, and so on) in the family size from year to year. This is according to R134(1.1)(a),R133(1)(j)(i)(B) and R2 (definition of the “minimum necessary incomeâ€), which is based on Statistics Canada’s LICO threshold, which takes into account the size of the family in a given year.

Counting increases and decreases to the family size for parent and grandparent applications

While increases and decreases in family size impact all sponsors and co-signers who must meet an income requirement, due to the number of years they must meet an income requirement, these changes are more likely to occur among sponsors and co-signers of parents or grandparents.

By assessing family size on a year-by-year basis, the family size may have increased within the 3 years preceding the date of the receipt of the sponsorship application. An officer is to include any marriages, common-law relationships and/or births for the year in which the increase to the family size occurred. For example, the sponsor had a newborn child and married in 2018. The sponsor submits a parent or grandparent application in 2019. The income requirements must be met for years 2016, 2017 and 2018. The sponsor’s spouse and newborn child must only be counted in the family size for the year 2018. However, if the sponsor’s spouse co-signs the application, the spouse must be included in all 3 years (please see Co-signers and non-co-signers of parent and grandparent applications for further details).

By assessing family size on a year-by-year basis, the family size may have decreased within the 3 years preceding the date of the receipt of the sponsorship application. An officer is to include any deceased family members, divorced family members, former common-law partner(s), former dependent children and/or previous undertakings in the family size for any year that the family members were part of the family size. For example, the sponsor’s father, who was married to the sponsor’s mother, passed away in 2018. The sponsor submits a parent or grandparent application in 2019 to sponsor their mother. The income requirements must be met for years 2016, 2017 and 2018. The sponsor’s father must be counted in the family size for years 2016 and 2017.

Co-signers and non-co-signers of parent and grandparent applications

A co-signing spouse or a co-signing common-law partner of the sponsor must be included in the family composition for all years. This means that officers must include the co-signer in all 3 relevant years when calculating family size, regardless of when the sponsor and co-signer married or became common-law partners.

Note: A sponsor’s separated spouse who is a Canadian citizen or permanent resident of Canada can co-sign a sponsorship application because they are considered to still be their spouse in all cases (even if in a common-law relationship with another person) until a divorce is granted. The common-law partner cannot co-sign in this instance.

If a sponsor’s separated spouse is a foreign national, the separated spouse cannot co-sign a sponsorship application, but is still considered their spouse unless the separated spouse is in a common-law relationship with another person.

A non-co-signing spouse or non-co-signing common-law partner of the sponsor must only be included in the family size calculation starting the year they married or became common-law partners. For example, a sponsor became a common-law partner in 2017. They submit a parent or grandparent application in 2019 with no co-signer. The income requirements must be met for years 2016, 2017 and 2018. As there is no co-signer on the application, the sponsor’s common-law partner must only be counted in the family size for 2017 and 2018.

Exception to minimum necessary income requirement

In general, a sponsor does not have to meet the MNI if they are sponsoring their spouse, common-law partner, conjugal partner, dependent child or a person under the age of 18 whom the sponsor intends to adopt in Canada [R133(4)]. However, in situations where an officer is of the opinion that the sponsor will be unable to provide adequate support and that the sponsored person will be unable or unwilling to support themselves and may have to rely on social assistance, the applicant may be found to be inadmissible for financial reasons [A39].

Note: If a dependent child sponsored as the principal applicant (or as a dependant of the principal applicant) has a dependent child, the MNI for the applicable family size has to be met. A sample scenario would be where someone is sponsoring their common-law partner who is accompanied by their 18-year old daughter and their daughter’s 2-year old child (the principal applicant’s grandchild).

Financial requirements for sponsors living in Quebec

Financial requirements are different for sponsors living in Quebec, and are assessed by the Quebec Ministère de l’Immigration, de la Francisation et de l’Intégration (MIFI), not by IRCC. Quebec establishes its minimum income figures based on the gross annual income required based on the Consumer Price Index published by Statistics Canada. Financial requirements for sponsors in Quebec are published on the financial capacity evaluation page of the MIFI website.

Quebec case at time of filing, but sponsor relocates outside of Quebec

For applications where the sponsor was a resident of Quebec at the time of filing, but has since moved outside of Quebec to another province or territory before a visa is issued and before le ministère de l’Immigration, de la Francisation et de l’Intégration (MIFI) has made their assessment, the sponsor will be advised that a financial assessment is required by IRCC.

For applications where the sponsor was a resident of Quebec at the time of filing, but has since moved outside of Quebec to another province or territory before a visa is issued, but after MIFI has made a positive assessment, the sponsor will be advised that a financial re-assessment is required by IRCC. This includes the initial 3 income years that were originally assessed and may include any subsequent 12-month period that has passed since the receipt of the application.

For both scenarios above, the sponsor will be advised that they may add their spouse or common-law partner as a co-signer. Centralized Network must request that the sponsor submit additional documents or information in order to add the co-signer to the application.

A co-signer may not be added to the sponsorship application if the sponsorship application was already assessed and the sponsor failed to meet the sponsorship requirements. A sponsor must be in compliance with the sponsorship requirements detailed in R133(1) (a) to (k) from the time the sponsorship and permanent residence applications were received by IRCC until the time that a final decision is made on both the sponsorship and permanent residence applications. For more detailed information, officers should refer to OB 324: Instructions to officers on adding a co-signer to a family class sponsorship undertaking, which is still active.

Reassessment of financial circumstances

A sponsor’s income can be reassessed prior to an initial recommendation being rendered on sponsorship eligibility, where information material to a sponsor’s ability to meet financial requirements is received by IRCC.

Income may be reassessed by IRCC [R134)(2)] only if either of the following applies:

- more than 12 months have passed since receipt of the application

- new information comes to IRCC’s attention that a sponsor may no longer be able to meet their financial obligations

The addition of a new family member to the application increases the family size. This will result in the need for the sponsor’s financial circumstances to be reassessed to ensure that the sponsor and co-signer (if applicable) continue to meet the MNI requirement.

Income requirements for sponsoring parents and grandparents

Sponsorship requirements for parents and grandparents are designed to ensure that sponsors provide evidence of their ability to provide long-term financial support. For sponsorship applications received by IRCC on or after January 1, 2014, sponsors and co-signers must meet or exceed the MNI of the LICO, plus 30% for each of the 3 taxation years immediately preceding the date of the application for which the CRA issues an NOA or Option C printout. Undertakings for parents and grandparents remain in effect for 20 years after the sponsored parent or grandparent (and any accompanying dependants) becomes a permanent resident.

Sponsors and co-signers have the choice to provide either of the following:

- their Social Insurance Number (SIN) and their consent to IRCC to obtain their income tax information directly from the CRA

- copies of their NOAs or Option C printouts in their application

Where a sponsor signs a statement of consent (question 8 on the Financial Evaluation for Parents and Grandparents Sponsorship) and provides their SIN, IRCC will obtain income tax information directly from the CRA. A sponsor who does not provide consent must complete the Income Sources for the Sponsorship of Parents and Grandparents form and submit an NOA issued to them by the CRA for each of the 3 taxation years immediately preceding the date of their application. Sponsors who do not have paper copies of NOAs can view (and print) their tax and income information using the CRA’s My Account online service.

The requirement to provide NOAs or Option C printouts for the 3 taxation years immediately preceding the date of their application is mandatory. Sponsors may not seek to maximize their income by providing 3 NOAs or Option C printouts of their choice or the 2 most recent NOAs or Option C printouts along with other evidence of income for the year they are applying before CRA makes these documents available. IRCC will only accept CRA issued documents for 3 tax years preceding the date of the application.

Note: Co-signers are required to meet the same requirements as sponsors, regardless of how long they have been married to or living in a common-law relationship with the sponsor. This means, for parent and grandparent applications, co-signers must also submit NOAs or Option C printouts for the 3 taxation years immediately preceding the date of the application in order for their income to be included in the MNI assessment.

R132(5) details the requirements to be a co-signer, R133 details the requirements to be a sponsor that also apply to a co-signer except for R133(1)(a), and R134 describes how the income of the sponsor and co-signer must be calculated. These provisions do not require that the sponsor or co-signer had to have been a permanent resident in the years for which their income is included, only that the sponsor or co-signer be a permanent resident of Canada or Canadian citizen at the time the application is submitted. This means that in cases where the sponsor and/or co-signer acquired permanent resident status part way through the 3 years immediately preceding the date of the sponsorship application, all 3 years (even if they were not a permanent resident during those years) should count toward the income requirements. See the subheading Assessing minimum necessary income for what income can be included in the MNI assessment.

Income requirements for sponsoring “other relativesâ€

Acceptable evidence of income is a copy of an NOA or Option C printout from the CRA for the most recent year available. Where an NOA or Option C printout is unavailable – for instance, if the sponsor has not recently filed an income tax return – or does not capture all income for the 12 months preceding the application, the CPC may consider letters from employers, pay statements or, if self-employed, contracts and receipts for services rendered.

For family class categories where the MNI requirements must be met, a sponsor cannot be found eligible if they fail to meet the MNI, even if they (and the co-signer, if applicable) have good employment prospects, considerable assets or other family members willing to provide additional support.

Application of the temporary public policies of the minimum income requirements for the 2020 and 2021 taxation years

The Temporary public policy concerning applications for permanent residence as a member of the family class whose sponsor must meet a minimum income requirement in 2020 and the Temporary public policy concerning applications for permanent residence as a member of the family class whose sponsor must meet a minimum income requirement in 2021 exempts certain permanent residence applicants from the requirement that their sponsor (and co-signer, if applicable) meet all of the requirements of the Immigration and Refugee Protection Regulations (IRPR) for the 2020 and 2021 taxation years respectively.

The 2020 public policy came into effect on October 2, 2020 and the 2021 public policy came into effect on December 23, 2021. Both public policies will end once no longer applicable.

Affected applications

These 2 public policies apply to the processing of all family class applications for permanent residence where the applicant’s sponsors must meet an income requirement when 2020 and/or 2021 income is/are assessed. This may include

- parents and grandparents applications received between January 1, 2021 and December 31, 2024

- any family class applications received prior to January 1, 2021 for which an officer has initiated a financial re-assessment

- non-parent and grandparent family class applications that are subject to an income assessment 12 months prior to the date of submitting the application

Regular employment insurance and the minimum necessary income requirement for 2020 and 2021 taxation years

Under these 2 public policies, all family class applicants’ sponsors (and co-signers, if applicable) who must meet income requirements will be able to count regular employment insurance benefits (which are normally subtracted) in their income calculations rather than just special employment insurance benefits for the 2020 and/or 2021 taxation year(s). Regular employment insurance benefits are included in the Total Income line 15000 (formerly line 150) of the NOA. The amount listed on line 13000 should not be excluded from eligible income for the 2020 and/or 2021 taxation year(s).

Sponsors (and co-signers, if applicable) must meet all other requirements of the Immigration and Refugee Protection Act (IRPA) and IRPR, except those for which an exemption is granted under these 2 public policies. Not all sponsors need to meet regulatory income requirements. Further details about which sponsors need to meet income requirements can be found under the section Exception to minimum necessary income requirement.

Parents and grandparents applications – Minimum necessary income assessment for the 2020 and 2021 taxation years

These 2 public policies allow foreign nationals applying for permanent residence as parents and grandparents to be exempted from the requirement for their sponsor to have the MNI plus 30% for the 2020 and 2021 taxation years, as long as the sponsor meets the MNI as defined in section R2 for the 2021 and 2021 taxation years, as well as all other applicable requirements, including those pertaining to the other relevant taxation years. In other words, these 2 public policies allow the principal applicant to be eligible for permanent residency even though their sponsor does not meet regulatory income requirements (as long as they meet the conditions outlined in the public policies for the 2020 and 2021 taxation years).

All parents and grandparents applications where a financial assessment on the 2020 and/or 2021 taxation year(s) is/are required will benefit from the lower income requirement of the applicable public policy or public policies. Sponsors (and co-signers, if applicable) still need to meet the MNI plus 30% for all other applicable taxation years, except for the 2020 and/or 2021 taxation year(s).

Officers should refer to the GCMS processing instructions below to determine whether the MNI has been met for the applicable taxation year. This example refers to the 2020 taxation year only, but it is also applicable for the 2021 taxation year.

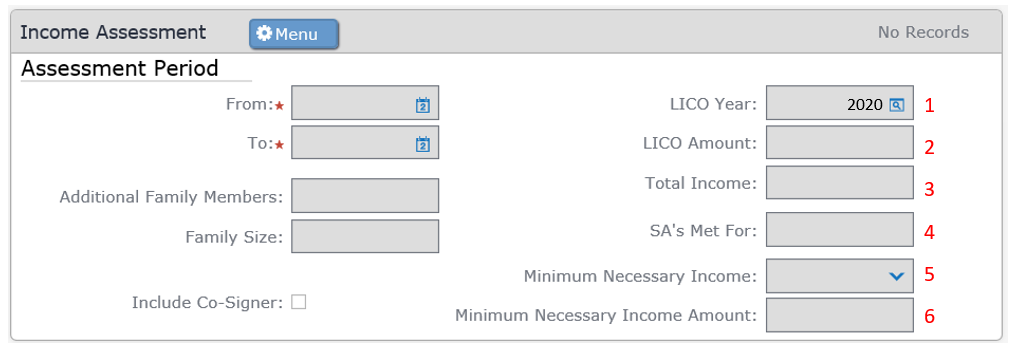

GCMS processing instructions

Under the “Sponsorship†tab and “FC Eligibility†sub tab, navigate to the “Income Assessment†sub screen in the tab.

The relevant GCMS fields are as follows (refer to the screenshot of the Income Assessment sub screen in GCMS):

- LICO Year: 2020

- LICO Amount

- Total Income: appears on line 15000 of the NOA or Option C printout

- SA’s Met For: family size

- Minimum Necessary Income: Met or Not Met

- Minimum Necessary Income Amount: (LICO + 30%)

Note:Â Prior to performing this assessment, the officer must ensure that all applicable income (including income under the Employment Insurance Act) for the sponsor (and co-signer, if applicable) is included in the 2020 and/or 2021 taxation year(s).

In order to apply the public policies, officers first have to find that sponsors do not meet the income requirements under the IRPR for the 2020 and/or 2021 taxation year(s). If sponsors meet the condition in the public policy or public policies, the principal applicant and their dependants (if applicable) may be eligible for permanent residency even though their sponsor does not meet the regulatory income requirements. The example in the instructions below do not apply to taxation years other than the 2020 taxation year.

The 3 steps below highlight the 3 different scenarios with next steps for each (assuming that the sponsors in question met the LICO + 30% for 2018 and 2019):

- First, verify whether the “Total Income†(#3) is equal to or greater than the “Minimum Necessary Income Amount†(#6). If it is, then the “Minimum Necessary Income†is “Met†(#5).

Result: Met without 2020 public policy: The “Total Income†(#3) is equal to or higher than the “Minimum Necessary Income Amount†(#6); the sponsor did not rely on the 2020 public policy.

- If the “Total Income†(#3) does not equal or exceed the “Minimum Necessary Income Amount†(#6), verify whether the “Total Income†(#3) is equal to or greater than the “LICO Amount†(#2). If it is, then the “Minimum Necessary Income†is “Met†(#5). Note: This GCMS field may need to be manually changed to “Metâ€.

Result: Met with 2020 public policy: The “Total Income†(#3) is equal to or higher than the “LICO Amount†(#2), but lower than the “Minimum Necessary Income Amount†(#6); the sponsor has benefitted from the 2020 public policy.

- If neither scenario above is applicable, then the “Minimum Necessary Income†is “Not Metâ€.

Result: Not Met: The “Total Income†(#3) is less than the “LICO Amount†(#2); the sponsor does not benefit from the 2020 public policy.

Summary of GCMS assessment

| Total income for the sponsor (and co-signer, if applicable) for the 2020 taxation year in GCMS | Does the sponsor meet the regulatory income requirements to sponsor? | Does the sponsor have sufficient income that the sponsored person could benefit from the public policy? |

|---|---|---|

| Higher than the “Minimum Necessary Income Amount†(#6) | Yes | Not applicable |

| Higher than the “LICO Amount†(#2), but lower than the “Minimum Necessary Income Amount†(#6) | No | Yes |

| Lower than the “LICO Amount†(#2) | No | No |

Family class sponsors who received COVID-19 benefits for the 2020 and/or 2021 taxation year(s)

Since some sponsors (and co-signers, if applicable) may have been affected financially by the COVID-19 pandemic, family class sponsors will be able to count the following benefits in their income calculation for the 2020 and/or 2021 taxation year(s):

- any Canada Emergency Response Benefits issued under the

- Employment Insurance Act or

- Canada Emergency Response Benefit Act

- other temporary COVID-19-related benefits

- as long as they are not part of provincial social assistance programs

Canada Emergency Response Benefits issued under the Employment Insurance Act or the Canada Emergency Response Benefit Act are not considered social assistance and will be included in line 15000 (previously line 150) of the NOA. COVID-19-related benefits are reported in line 13000, which in turn is included in line 15000. Since line 15000 includes federal COVID-19 benefits, there is no requirement for an officer to identify and add an amount to the income calculation.

Any amount appearing on line 14500 is considered social assistance. Since the CRA includes line 14500 in the total income (line 15000), officers must subtract this amount from line 15000 to comply with the requirement under subparagraph R134(1)(c)(ii) and subparagraph R134(1.1)(b)(ii) to exclude social assistance received by the sponsor from a province from the income calculation. For other temporary COVID-19-related benefits, if a province or territory has determined that their benefit is considered social assistance, IRCC will agree with the province or territory’s interpretation and also treat the benefit as such. The assessment of social assistance continues to be the same as before the application of this temporary public policy. As a reminder, as per paragraph R133(1)(k), a sponsorship application can only be approved by an officer if, from the day on which the application has been filed until the day a decision is made, the sponsor is not in receipt of social assistance for a reason other than disability.

Duration of sponsorship undertakings

The undertaking takes effect on the day the sponsored person becomes a permanent resident. The lone exception is sponsored persons who hold a temporary resident permit (TRP).

For sponsored foreign nationals who were issued a TRP under A24 following an application for a permanent resident visa, the undertaking takes effect on the day they enter Canada or, if they are already in Canada, on the day on which they obtain the TRP following their application to remain in Canada as a permanent resident [R132(1)(a)(ii)].

Sponsors and co-signers remain responsible for the sponsored person throughout the period of temporary resident status and continue their sponsorship responsibility throughout the specified period of the undertaking, commencing on the day the applicant becomes a permanent resident.

For cases where a family class application is refused and a TRP is subsequently issued, there is no obligation on the part of the sponsor to provide support.

Because the application was not approved, there is no undertaking in effect. Therefore, any social assistance received during the period the sponsored person is in Canada on a TRP is not subject to default or collection.

| Category | Code | Duration of undertaking | Regulation |

|---|---|---|---|

| Spouse | FC1 | 3 years | R132(1)(b)(i) |

| Common-law Partner | FCC | 3 years | R132(1)(b)(i) |

| Conjugal Partner | FCE | 3 years | R132(1)(b)(i) |

| In-Canada Spouse and Partner Public Policy | FCH | 3 years | R132(1)(b)(i) |

| Dependent Child and accompanying children of spouses and partners | FC3 | Child under 22: 10 years or until child turns 25 Children 22 years of age or older: |

R132(1)(b)(ii) R132(1)(b)(iii) |

| Parent or Grandparent and accompanying children of parents or grandparents | FC4 | Sponsorship received before January 1, 2014: 10 years Sponsorship received after January 1, 2014: |

R132(1)(b)(iv) |

| Orphaned brother, sister, nephew, niece or grandchild | FC5 | 10 years | R132(1)(b)(v) |

| Child to be adopted [R117(1)(g)] | FC6 | Children under 22: 10 years or until child turns 25 |

R132(1)(b)(ii) |

| Other relative | FC7 | 10 years | R132(1)(b)(v) |

| Adopted child [R117(2) and (3)] | FC9 | Children under 22: 10 years or until child turns 25 Children 22 years of age or over: |

R2 R132(1)(b)(ii) R132(1)(b)(iii) |

Duration of undertakings – Quebec

An undertaking made by a sponsor who resides in Quebec (or who lives outside Canada but intends to reside in that province) is a binding contract between sponsors (and co-signers, where applicable) and the province of Quebec [R131(b)]. The Canada-Quebec Accord and the Immigration and Refugee Protection Regulations give Quebec responsibility for setting some of its own eligibility criteria for sponsors and for administering undertakings. IRCC does not process or administer Quebec undertakings.

The Canada-Quebec Accord gives Quebec responsibility for setting its own criteria for family class sponsorship and administering undertakings.

Quebec is responsible for

- administering sponsorship undertakings

- determining the financial criteria for the sponsorship of foreign nationals intending to live in Quebec

- determining the duration of an undertaking

- addressing sponsorship defaults

- issues related to a sponsor’s court-ordered support obligations or personal bankruptcy

Note: Quebec will not accept an undertaking from a sponsor who does not reside in Quebec, unless the sponsor is a Canadian citizen abroad and intends to reside there once their sponsored family member becomes a permanent resident. A sponsor who resides in another province when they submit a sponsorship application but plans to move to Quebec once their sponsored relative becomes a permanent resident must inform IRCC of their intention so that the CPC can instruct the sponsor of procedures to follow to meet provincial requirements. In such cases, the CPC would liaise as needed with MIFI. A sponsor who moves to Quebec during processing is similarly required to advise the office processing the application.

A sponsor who signed an undertaking with the province of Quebec but who moves from Quebec to another province while their application is in process is required to complete and submit a new IMM 1344 Sponsorship Application to Sponsor, Sponsorship Agreement and Undertaking and submit it to the CPC, where it will be assessed based on federal requirements. This includes determining whether the sponsor meets the MNI requirements.

| Person sponsored | Duration of undertaking |

|---|---|

| Spouse, common-law partner, conjugal partner | 3 years |

| Child under 16 years of age | 10 years or until the child turns 18, whichever period is longer |

| Child 16 years or over | 3 years or until the child turns 25, whichever period is longer |

| Any other relative | 10 years |

See up-to-date information on the duration of Quebec undertakings on the MIFI website.

Co-signers

A spouse or common-law partner may co-sign an undertaking to help meet the MNI requirements by pooling financial resources (for example, to meet the MNI when sponsoring a parent or grandparent, a grandchild or “other relativeâ€). No other family member can co-sign. An eligible co-signer’s income can be included for the purpose of meeting financial requirements, but not when the co-signer is the person being sponsored (that is, the sponsor’s spouse, common-law partner or conjugal partner). No other family member’s income or resources can be included by the sponsor for this purpose.

In order to be a co-signer, at the time of signing the undertaking, a sponsor’s common-law partner must have cohabited with the sponsor in a conjugal relationship for at least one year. There is no time limit for living together for a spouse to be a co-signer. There is no need for a co-signer in cases where the sponsor alone meets the MNI requirements or where financial requirements are not applicable.

In cases with a co-signer where the sponsor’s income alone is sufficient to meet the MNI and there is the possibility that processing may need to be suspended in order to investigate the co-signer’s eligibility, an officer should contact the sponsor and recommend that the co-signer withdraw to prevent unnecessary delays. This will prevent unnecessary delays and the possibility of a negative sponsorship eligibility decision.

Use of a co-signer is applicable to applications to sponsor the following family members:

- parents and grandparents

- dependent children, in cases where their dependent child (that is, a grandchild) is included on the application as an accompanying dependant

- “other relatives†[R117(1)(h)]

A person who is married to another person will continue to be the “spouse†of that person within the meaning of R132(5) until a divorce granted in Canada under the Divorce Act takes effect or, if the divorce was granted outside of Canada by a competent authority, it is recognized pursuant to the Divorce Act. This means that even if the sponsor is separated from their spouse, unless they are legally divorced, they are still considered spouses and, therefore, a separated spouse can co-sign the sponsorship application.

A co-signer is equally responsible as the sponsor to provide basic requirements: food, clothing, shelter, fuel, utilities, household supplies, personal requirements, and other goods and services, including dental care, eye care and other health needs not provided by public health care to the sponsored person. At the same time, the applicant agrees to make reasonable efforts to provide for their basic requirements and those of their family members.

Adding a co-signer during processing

A co-signer can be added between the day on which the sponsorship application was filed and the day on which a decision is made with respect to the application, if required, due to a change in circumstances related to family composition and the need to meet the increased MNI for the increased family size.

When assessing the sponsor’s income, an officer will consider both the increase in the MNI requirements resulting from the addition of a co-signer to the family size and the co-signer’s income, calculated in accordance with R134(a) to (c) against the LICO in effect at that time. This is in line with the Federal Court ruling in Dokaj vs. Canada, that if an officer considers an applicant’s spouse or partner in the calculation of the size of the applicant’s family, that person’s income should also be included in the financial assessment.

If the combined income of the sponsor and the added co-signer is not at least equal to the LICO, or the income is not from a Canadian source and is not included in the NOA, the sponsor does not meet the income requirement, and is deemed to be ineligible.

Note: Except in instances where there is a change in family circumstances, a co-signer may not be added to the sponsorship application if the sponsorship was already assessed and at the time of that assessment, the sponsor failed to meet the sponsorship requirements. R133(1) requires that a sponsor be in compliance with the sponsorship requirements detailed in R133(1)(a) to (k) from the time the application was received by IRCC until the time that a final decision is made on their application.

Co-signers are not sponsors

If a sponsor withdraws, co-signers may not continue with a sponsorship. If a co-signer wishes to continue the application as the sponsor, they can submit a new application – only if the person being sponsored also meets the definition of a member of the family class – which IRCC will assess independently. For example, a sponsor’s spouse or partner cannot submit an undertaking for the sponsor’s parent or grandparent if the sponsor withdraws.

In the event of a refusal of a sponsored family class member, co-signers do not have a right of appeal. That right is exclusive to the sponsor. For example, a person who co-signs their spouse’s sponsorship of their parents cannot appeal a refusal of the permanent resident visa of their in-laws.

Sponsorship default

Sponsors (and co-signers) are in default of an undertaking if the sponsored person receives social assistance during the validity period of the undertaking. Unless the sponsor (and/or co-signer) or the sponsored person repays the government that has provided social assistance, sponsors (and co-signers) are not eligible to sponsor any other member of the family class. The death of a sponsored applicant does not nullify default of an undertaking.

Provinces and territories (P/Ts) may seek to recover social assistance payments made to a sponsored member of the family class or their family members (including social assistance for reasons of disability) from the sponsor and/or co-signer. If the sponsor dies, the co-signer, if applicable, is responsible for the deceased sponsor’s obligations. Until the co-signer repays the sponsorship debt/obligation the co-signer will remain in default of the undertaking. Where there is no co-signer, the decision as to whether to collect from a deceased sponsor’s estate rests with the government that is responsible for the debt collection.

In Canada, social assistance benefits are administered provincially. The IRPR (R2) define social assistance in broad terms, but render someone who is in receipt of social assistance for a reason other than a disability ineligible to be a sponsor under the family class [R133(1)(k)]. The intent of R133(1)(k) is to bar persons whose primary or sole source of income is “social assistance†benefits from sponsoring a relative under the family class. There are various programs and services provided by P/Ts that confer benefits that IRCC does not consider to be social assistance for the purposes of imposing a bar on sponsorship.

Examples of these would include, but are not limited to:

- subsidized housing

- tax credits

- child care subsidies

- other benefits that would be widely available to residents of a P/T, including persons who are employed

If a sponsor resumes providing for a sponsored member of the family class who had been, but is no longer in receipt of social assistance, they are still in default until such time as social assistance authorities in the P/T confirm that the debt has been repaid in full.

Sponsorship withdrawal

On the IMM 1344 Application to Sponsor, Sponsorship Agreement and Undertaking form, a sponsor is required to indicate, if they are found ineligible to sponsor, that they choose either of the following scenarios:

- they withdraw the sponsorship application

- they allow IRCC to continue with an assessment of their relative’s application for permanent residence

A family class sponsorship case can be closed by the CPC without a final decision being made on the application for permanent residence when one of the following occurs:

- the sponsor is found to be ineligible to be a sponsor, and indicated in Part 1, Question 1 of the IMM 1344 that their choice was to withdraw the sponsorship application

- the sponsor requests to withdraw the sponsorship

The CPC must enter information in GCMS stating that the case has been closed. When no decision has been made regarding issuance of a permanent resident visa, the sponsor has no right of appeal.

When a sponsor withdraws the application, the CPC will refund both:

- the right of permanent residence fee (RPRF), if it has been paid

- the application for permanent residence fee, if processing of the application for permanent residence has not already begun

Note: The sponsorship fee can be refunded only in cases where the sponsor requests to withdraw the application before IRCC starts processing it.

A sponsor who is found eligible but who contacts IRCC in writing, seeking to withdraw the undertaking before processing has started on the application for permanent residence, is eligible to receive a refund of the permanent residence fee. There is no refund of the sponsorship fee.

A sponsor who requests to withdraw a sponsorship undertaking after the processing of the sponsored relative’s or family member’s application for permanent residence has started is not eligible for a refund of the permanent residence fee, nor do they have a right to an appeal.

If a sponsor withdraws once processing has begun, the application for permanent residence will be closed. Permanent residence cannot be granted to foreign nationals applying as members of the family class and their dependants where a valid sponsorship undertaking is not in effect [R120].

A request to withdraw a sponsorship cannot be accepted if the sponsored person has already become a permanent resident.

A sponsor has the right to withdraw at any time during processing of either the sponsorship application or the application for permanent residence up until the sponsored family member has been granted permanent residence at a port of entry (POE) or at a local IRCC office. This includes the right to withdraw the sponsorship of a family member who has been issued a Confirmation of Permanent Residence (COPR) and, where applicable, a permanent resident visa, based on a positive final decision, but who has not yet been granted permanent residence by an officer at a POE or in Canada.

IRCC cannot refuse to accept a sponsorship withdrawal request for a sponsored family member who has not yet become a permanent resident. The sponsored family member(s) cannot dispute the withdrawal.

A sponsor who wishes to withdraw must submit a notification to IRCC by web form – a sponsor is not obligated to provide IRCC with the reason(s) why they are requesting to withdraw. A sponsor cannot withdraw their support after the sponsored family class member has become a permanent resident. In such cases, the sponsor is bound by the undertaking, and remains responsible for their relative for the duration specified for the applicable family class category.

Co-signer withdrawal

A co-signer has the right to withdraw at any time during processing of either the sponsorship application or the application for permanent residence up until the sponsored family member has been granted permanent residence at a POE or at a local IRCC office. This includes the right to withdraw the sponsorship of a family member who has been issued a COPR and, where applicable, a permanent resident visa, provided they have not yet become a permanent resident.

A co-signer who wishes to withdraw must submit a notification to IRCC by web form. A co-signer cannot withdraw their support after the sponsored family class member has become a permanent resident. In such cases, the co-signer is bound by the undertaking, and remains responsible for their relative for the duration specified for the applicable family class category. A co-signer who withdraws prior to the granting of permanent residence and has been removed from the undertaking is not obligated to provide support to the sponsored family member.

In cases where a sponsor has withdrawn, processing of the application cannot continue, even if there is a co-signer who independently meets sponsorship requirements. If the principal applicant is a family class relative of the co-signer, the co-signer has the option of sponsoring only if a completely new sponsorship and permanent residence application is submitted and would be expected to meet the applicable requirements, including, where applicable, meeting the MNI requirements.

Note: In the event that the sponsor has a new spouse or common-law partner (which may be the reason for the co-signer withdrawal) that person can co-sign the new IMM 1344. If this is a common-law relationship, the officer should be satisfied that it has existed for at least one year. This is only allowed in cases where the original MNI assessment (where applicable) was passed.

Quebec sponsorship or co-signer withdrawal

See more information at: Applications under family classes: Sponsorships from persons residing in Quebec: Sponsor chooses, “to withdraw your sponsorship†if found ineligible to sponsor

Assessing a sponsor’s eligibility

Requirements in R130 to assess sponsor’s eligibility

To be eligible, a sponsor must provide proof that they are at 18 years of age or older, and either a permanent resident of Canada, a Canadian Citizen or a Status Indian.

Acceptable proof of permanent residence is a photocopy of a permanent resident card (PR card) or a record of landing [IMM 1000] if they have never obtained a PR card.

Acceptable proof of Canadian citizenship is a photocopy of one of the following:

- a Canadian Citizenship certificate or card (both sides)

- a Canadian birth certificate issued by the relevant provincial or territorial authority (for Quebec, must be one issued by the Directeur de l’état civil du Québec)

- the bio-data page of a Canadian passport

Acceptable proof of being a Status Indian is a photocopy of an Indian status card verifying registration in Canada as an Indian under the Indian Act.

Information may also be available in GCMS to confirm a sponsor’s status.

A sponsor must be residing in Canada, unless they are a Canadian citizen residing abroad sponsoring a spouse, common-law partner, conjugal partner or dependent child (provided that the dependent child does not have dependent children of their own) [R130(2)].

See Sponsorship by Canadian citizens living abroad

Sponsors who maintain a principal residence in Canada are not considered to be in violation of residency requirements if they

- take short holidays or business trips outside Canada on a temporary basis

- have work arrangements that require them to be outside Canada for temporary finite periods of time, but return to live in Canada in between assignments (such as ship crew or seasonal workers)

Persons who do not maintain a principal residence in Canada and who live and work abroad and only return to Canada for short visits are not considered to meet residency requirements.

Sponsorship by Canadian citizens living abroad

The only exception to the requirement for a sponsor to reside in Canada is a Canadian citizen residing abroad who sponsors a spouse, common-law or conjugal partner, or dependent child (who does not have a dependent child of their own) and who intends to return to reside in Canada once their sponsored relative becomes a permanent resident [R130(2)]. If a child has not been adopted yet, they are not considered a dependent child pursuant to the Regulations.

Sponsorship ineligibility identified at the permanent resident processing stage

A sponsor must be eligible from the day the sponsorship application is received by IRCC until the sponsored person becomes a permanent resident. When a processing officer suspects that a sponsor deemed eligible by the CPC is, in fact, ineligible, as a designated decision maker, they must do all of the following:

- review information provided by the sponsor and co-signer

- verify in GCMS whether the sponsor/co-signer is subject to any of the applicable bars